Written by Ganesh Kompella on Digilah (Tech Thought Leadership)

In the wake of recent crypto events, I feel it necessary to write an opinion piece on what stablecoins are, why they exist and what separates them from being good or bad.

What is a stablecoin?

A stablecoin is a crypto asset pegged to a real-world asset’s value.

Example: 1 USDT is always intended to be worth 1 US dollar. They hold their value relative to traditional currencies but, unlike the money in your bank account, they can be used freely on the blockchain.

Similar to traditional currencies, these stablecoins can be used for buying, selling, sending, and lending within the crypto markets.

In terms of timeline – USDT was the very first crypto stablecoin, then Circle introduced USDC, Binance introduced BUSD, Luna introduced the failed algo stablecoin UST and there are a bunch of others.

How are they different from regular currency?

Stablecoins are more cost- & time-efficient than the decades-old payment rails that the financial system relies on.

They are transferable 24/7/365 & are faster & cheaper to transact with than fiat. That’s why they continue to rise in popularity through bull and bear markets.

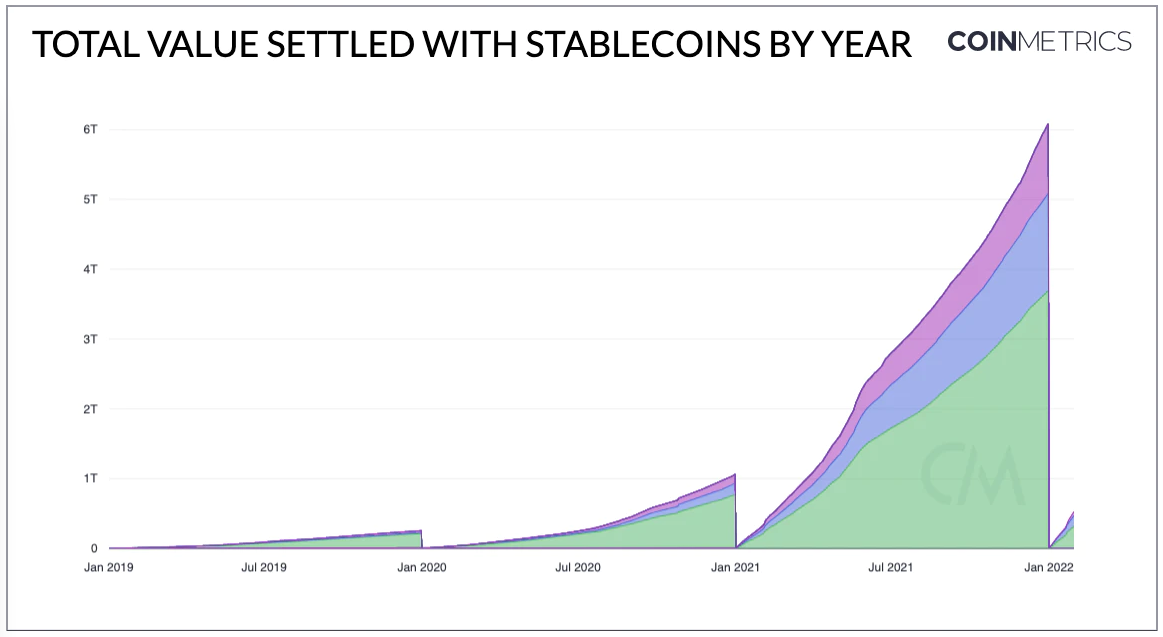

In 2021 alone the total value settled with stablecoins was $6T, up 600% from its 2022 high of $1T. This graph from CoinMetrics sheds a light on how popular these are becoming.

Different types of Stablecoins

There are essentially three types of stablecoin designs:

- Fiat-collateralized

- Crypto-collateralized

- Algorithmic

The mechanics of each are different from one another as the names suggest, some are asset backed while some are code backed. They work very differently from one another and have distinctive pros and cons amongst themselves.

Fiat-collateralized

Fiat backed stablecoins work very much like regular money market funds. You deposit your dollar with a stablecoin entity and get an equivalent amount of stablecoins in return.

Let’s take USDT (Tether) as an example.

A $100 deposit will get you $100USDT. You get the stablecoin and you are free to use it anyway you choose onto any of the blockchain networks that support tether. And the issuer puts your deposit to use and earns interest. With a crucial promise that you can always go back to the issuer, redeem your USDT for U.S.Dollars.

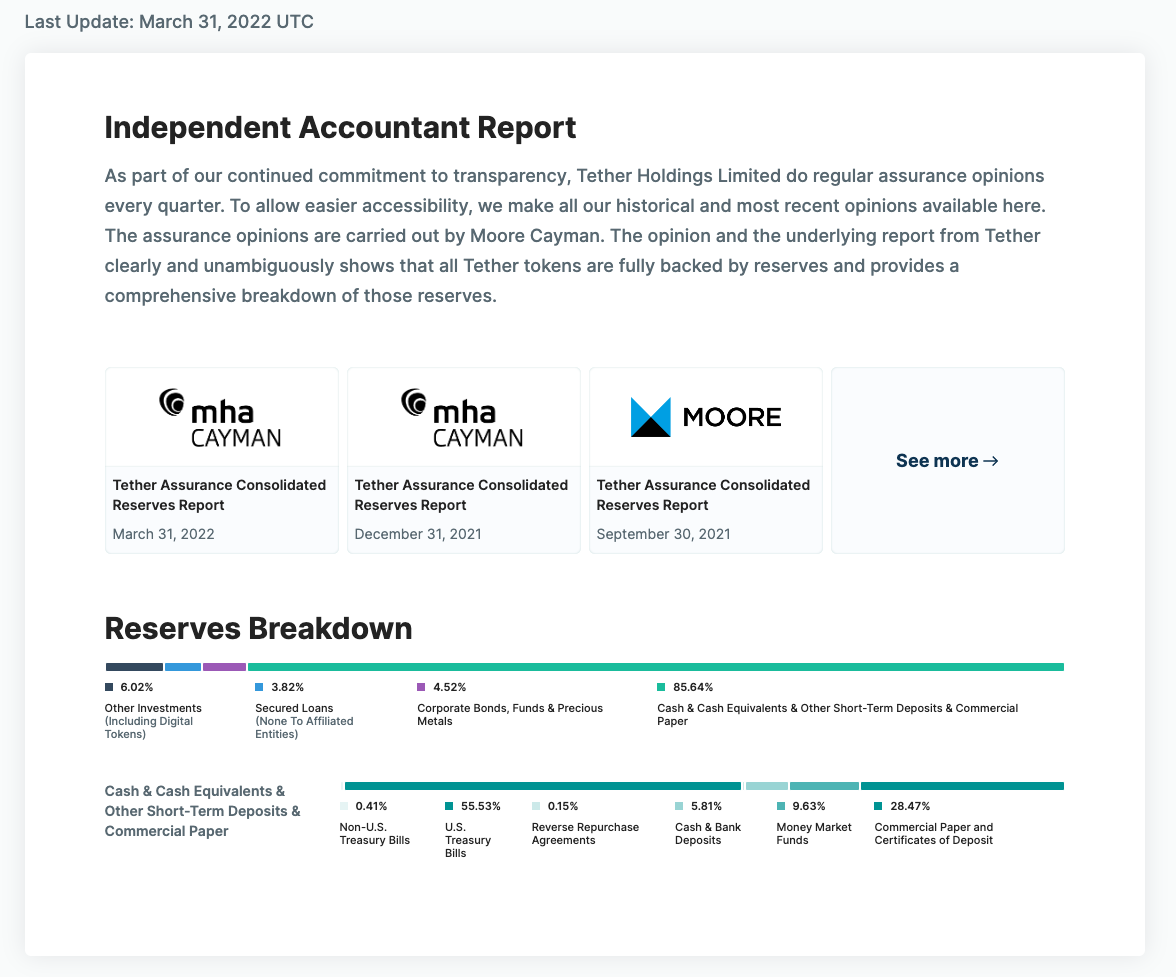

Diving into Specifics, this is how Tether manages their deposit reserves (Last reported on March 31, 2022). Your deposits turned reserves are mostly into Cash & Cash equivalent with some allocations into other asset classes like secured loans, corporate bonds, and digital tokens. These entities get audited from time to time.

As an investor you must take notice of these audits, review them, and make an assessment on the issuer’s reserves. Strong reserves indicate they wouldn’t have any liquidity concerns in the event of a market crash or bank run.

Crypto-collatarized

Crypto-backed stablecoins operate more like traditional home equity loans. Investors deposit crypto with a decentralized issuer (usually a DeFi protocol), which issues stablecoins in exchange.

The investor must repay the stablecoins (plus a fee) to redeem their crypto assets. The critical promise is that every crypto-backed stablecoin in circulation is directly backed by excess collateral.

From a transparency perspective, the reserves can be audited & monitored by anyone in real time (including regulators). They just need to look on-chain. $DAI is an example of such stablecoin. It’s trusted by a huge community of crypto investors and developers.

Algorithmic stablecoins

They are typically minted & issued by a DeFi protocol and are commonly under-collateralized (meaning they aren’t backed by an equivalent or excess amount of collateral). Instead, they mostly rely on an algorithm that aims to maintain a stable price by expanding & contracting the stablecoin’s supply.

The intent is to influence interest rates and market behavior, which, in theory, ultimately return the stablecoin to its target price. The key promise is that the algorithm & incentive mechanisms work as promised, & the stablecoin maintains its peg through the issuance & removal of its supply.

The downside: The non-collateralized, algorithmic model keeps failing. Luna UST is one such example.

Historically, the adoption of Fiat-collaraterized stablecoin has dominated this segment, with over 95% of the market share, some economists even call it “Smart Money”.

What does the future hold?

Stablecoins definitely have the potential to play a pivotal role in the global economy and the future of digital finance.

Once we see central banks, regulators and the traditional financial sector starting taking notice which they already have. They could bring a host of benefits into this sector.

The pros of stablecoins are obvious: Low-cost, safe, real-time and more intuitive and competitive with what the consumers and businesses need today.

They could rapidly change and make it cheaper for businesses to accept payment, for governments to run cash intensive programs and connecting the unbanked population.

MOST SEARCHED QUESTION

What is the point of stablecoins?

Can you make money on stablecoins?

How many stablecoin are there?

MOST SEARCHED QUERIES

Stablecoins list

Best stablecoin

Is Bitcoin a stablecoin

For more such amazing content like and follow Digilah