Miners perform cryptographic hashes (two successive SHA256) on what is called a block header.For each new hash, the mining software uses a different random number called the nonce. The nonce is an integer value with 32 bits of memory allocated to it.

This means that it is limited to only around 4 billion possibilities, which with the network’s current hashing power is largely insufficient. We therefore add in the hash timestamp of the block in Posix time , constantly updated. Another variable element on which minors can play: the arrangement of transactions.

Including the block number, timestamp, nonce, block data and hash of the previous block, the hash produced will look like this:

This hash can be converted into a very long number. (It is a hexadecimal number, which means that the letters AF are the numbers 10-15). To make mining difficult, there is something calledtarget difficulty.

To create a valid block, a miner must find a hash that is below the target difficulty. For example, if the difficulty is:

Because the target is a bulky number with many digits, a simpler number is usually used to express the current target. This number is called the mining difficulty.Mining difficulty is scaled to the first block created. Which means that a difficulty of 70,000 means 70,000 times more computing power than it took Satoshi Nakamoto to generate the first block, when he was the only miner and only using the CPU of a computer.

When mining a block, miners include a timestamp in the block. Since 2016, this ” timestamp ” allows the network to adjust to the passage of time by calculating the median time spent (MTP), that is to say the median of the timestamps of the last 11 blocks. To be valid, a timestamp cannot be more than two hours in the future relative to the node’s subjective time.

The difficulty changes every 2016 block. The network adjusts the difficulty so that the generation time of these 2016 blocks is 14 days, regardless of the computing power deployed.

Therefore, the difficulty follows the power of the network. The adjustment algorithm is as follows: if the time measured in the period of 2016 blocks is less than 20,160 minutes (expected time), then the difficulty increases to comply with the assumed computing power; if it is higher, then the difficulty decreases. Retargeting is limited to a factor of 4 (multiplication as division) to avoid instabilities.

Most searched question

What is cryptocurrency?

What is bitcoin and how does it work?

Most searched queries

Ethereum price

Bitcoin price

Hello readers! Hope you liked what you read today. Click the like button at the bottom of this page and share insights with your colleagues and friends!

There is a palpable sense of skepticism in many with regards to the promise of inclusivity in Web3. Many believe that all talk of decentralization is a mere hype and is not implementable.

When one looks at the Metaverse players across various layers and that the metaverse market is projected to be worth $12Tn by 2030, the values of pay-parity, equity and inclusivity need to be lived in and by the Metaverse players.

Are there companies working on inclusivity and equity in places like Africa and economically backward countries?

Are there real possibilities to generate revenue and employment for the deprived or underprivileged classes of our society, with Web3 technologies?

The internet had made similar promises in the beginning and the utopian dream died within years of its inception. If we look at the internet today, there are pockets of improvement in revenue generation in rural and tribal populations but largely, it has skewed more, making the privileged a little more privileged.

Hence, considering the promise of Web3 in decentralization and self-sufficiency in revenues, this article attempts to provide scenarios across various layers of Metaverse as depicted below, to make this utopian ideal a reality.

The Artisan Community and Indian Craft

As an ancient civilization that has birthed many cultures and has seen numerous migrations and invasions, India has a rich heritage in the field of arts.

Craft as a term was historically limited to “goods worked by hand” but now includes a broader canvas – all things art, like Music, Dance, Painting, Sculptures, Textiles etc. Even if we limit Indian craft to “Handicrafts” across states, the variety in art form and media is unparalleled.

The Export Promotion Council for Handicrafts (EPCH) is a nodal agency for promoting exports of handicrafts from India to various destinations of the world and projecting India’s image abroad as a reliable supplier of high-quality handicrafts goods & services.

The Handicrafts exports during the year 2021-22 was Rs.33253.00 Crores (US$4459.76 Million) registering a growth of 29.49% in rupee terms & 28.90% in dollar terms over previous year1. While the growth is promising especially from a tourism perspective, this may have a miniscule impact on the overall rating of India as the Vishwaguru.

Revenue Generation for Artisans, while preserving the Art Heritage

The fast-paced Digital Age is only going to get faster with Industry 4.0. With technologies like VR/AR, 3D-Scanning and 3D-Modeling, 3D-Printing as well as Web 3.0 constructs (and buzzwords) like the NFT, Metaverse and Blockchain, the craft Industry has all the components aligned for that leapfrog moment.

A lot of artisan communities and tribal art communities in India are now extinct and some on the verge of extinction – this is a challenge that uniquely presents itself to us as an opportunity if we leverage the technologies mentioned above.

Industry 4.0 terms Technology as a driver of change, and not merely an enabler. We should look to harness this driver for Indian Craft and the numerous communities associated with it.

There is a need to look at Indian Craft holistically, including all forms of fine art and performing arts, compounded by technology and tourism. We Illustrate these possibilities by taking the famous Channapatna Toys from Karnataka, as an example. They are protected as a Geographical Indication (GI) under the World Trade Organisation administered by the Government of Karnataka.

Channapatna Toys could be put up on an artisan marketplace in the Metaverse. The artisan would be able to directly engage in selling goods in 3D and voice-interact with consumers worldwide. With technologies like 3D-scanning and 3D-printing, consumers worldwide would be able to see, touch and feel these products via Haptic technologies and also view the story of the artisan behind it.

Such multi-sensory experiences are disruptive and could help consumers in accelerating their buying decisions, something the Internet has not been able to achieve.

Consumers will not only get to pick up local artisans’ produce but also engage with them and know more about our culture, traditions and heritage from their standpoint. The same product, once digitized, could be converted to limited edition NFTs during special seasons. The underlying financial technology could be powered by Digital Ledger Technology (DLT) or Blockchain, keeping the transaction decentralized, bereft of middle-men.

Imagine the access for the artisans to the entire Indian Diaspora across the world and imagine the ease of access and purchase for the consumers, at large. This will also help the Artisans transfer knowledge to the next generation, a large number of who are looking for better economic opportunities in cities.

As mentioned earlier, this is the main reason why India has lost a lot of tribal and native art. With metaverse and ancillary technologies, the hope is that we will be able to reverse this trend and preserve art heritage for posterity while making it economically viable for the artisans at scale, something that is unknown and unprecedented in today’s times.

Early traction in such technology-driven soft power can certainly propel India onto the world stage and make traditional Indian artisans global celebrities, giving them the much needed recognition and respect.

Conclusion

Indian Heritage and Culture is multi-layered, with each layer having the capability to catapult India’s soft-power quotient. One could experience it through ancient monuments, scriptures, textiles, crafts, music, dance, food, sports, folktales and many more.

There is a need to look at each of these layers from a Technology and Tourism standpoint, the intent being to preserve and propagate Heritage and Cultures of the world, including the most backward communities.

If deployed across other art-forms like paintings, pottery, sculptures, textiles, and even artists like musicians and dancers, Artisans worldwide have tremendous potential to earn from a global market without boundaries.

Hello readers! Hope you liked what you read today. Click the like button at the bottom of this page and share insights with your colleagues and friends!

In the wake of recent crypto events, I feel it necessary to write an opinion piece on what stablecoins are, why they exist and what separates them from being good or bad.

What is a stablecoin?

A stablecoin is a crypto asset pegged to a real-world asset’s value.

Example: 1 USDT is always intended to be worth 1 US dollar. They hold their value relative to traditional currencies but, unlike the money in your bank account, they can be used freely on the blockchain.

Similar to traditional currencies, these stablecoins can be used for buying, selling, sending, and lending within the crypto markets.

In terms of timeline – USDT was the very first crypto stablecoin, then Circle introduced USDC, Binance introduced BUSD, Luna introduced the failed algo stablecoin UST and there are a bunch of others.

How are they different from regular currency?

Stablecoins are more cost- & time-efficient than the decades-old payment rails that the financial system relies on.

They are transferable 24/7/365 & are faster & cheaper to transact with than fiat. That’s why they continue to rise in popularity through bull and bear markets.

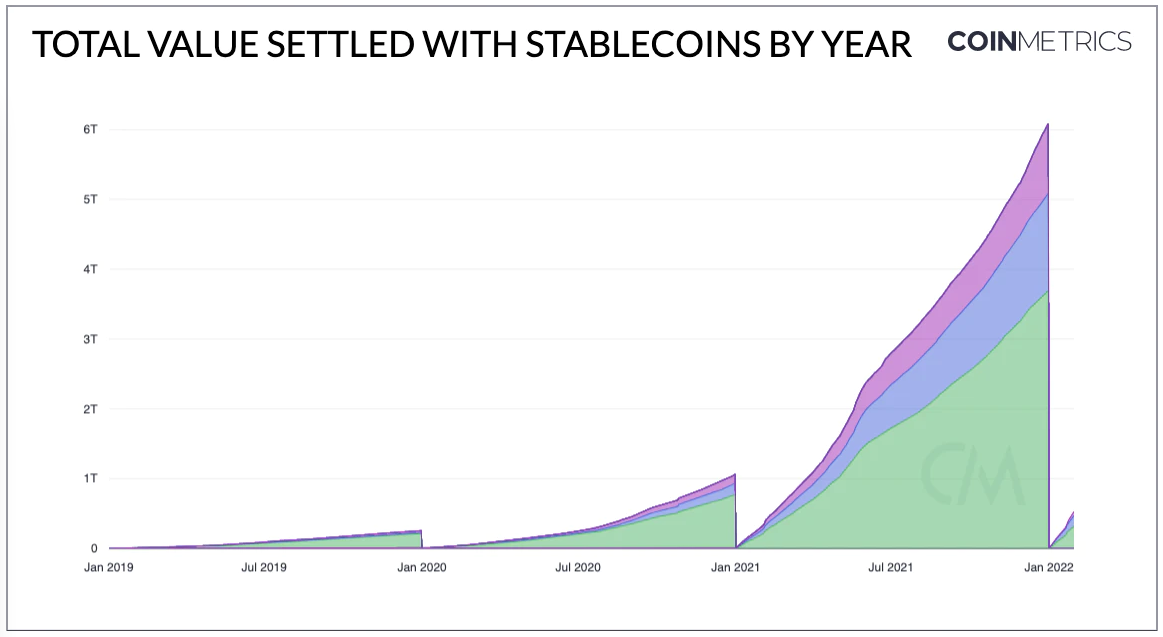

In 2021 alone the total value settled with stablecoins was $6T, up 600% from its 2022 high of $1T. This graph from CoinMetrics sheds a light on how popular these are becoming.

Different types of Stablecoins

There are essentially three types of stablecoin designs:

Fiat-collateralized

Crypto-collateralized

Algorithmic

The mechanics of each are different from one another as the names suggest, some are asset backed while some are code backed. They work very differently from one another and have distinctive pros and cons amongst themselves.

Fiat-collateralized

Fiat backed stablecoins work very much like regular money market funds. You deposit your dollar with a stablecoin entity and get an equivalent amount of stablecoins in return.

Let’s take USDT (Tether) as an example.

A $100 deposit will get you $100USDT. You get the stablecoin and you are free to use it anyway you choose onto any of the blockchain networks that support tether. And the issuer puts your deposit to use and earns interest. With a crucial promise that you can always go back to the issuer, redeem your USDT for U.S.Dollars.

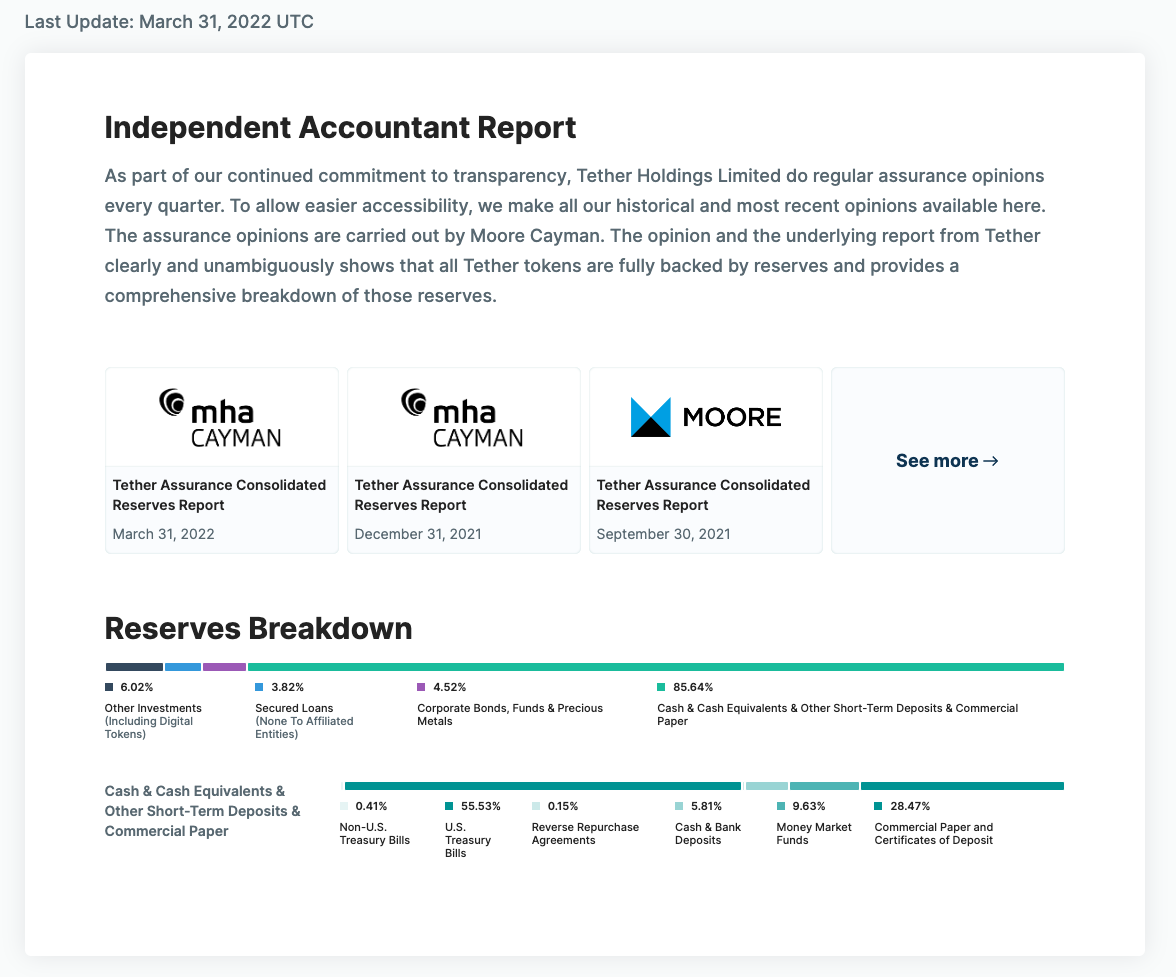

Diving into Specifics, this is how Tether manages their deposit reserves (Last reported on March 31, 2022). Your deposits turned reserves are mostly into Cash & Cash equivalent with some allocations into other asset classes like secured loans, corporate bonds, and digital tokens. These entities get audited from time to time.

As an investor you must take notice of these audits, review them, and make an assessment on the issuer’s reserves. Strong reserves indicate they wouldn’t have any liquidity concerns in the event of a market crash or bank run.

Crypto-collatarized

Crypto-backed stablecoins operate more like traditional home equity loans. Investors deposit crypto with a decentralized issuer (usually a DeFi protocol), which issues stablecoins in exchange.

The investor must repay the stablecoins (plus a fee) to redeem their crypto assets. The critical promise is that every crypto-backed stablecoin in circulation is directly backed by excess collateral.

From a transparency perspective, the reserves can be audited & monitored by anyone in real time (including regulators). They just need to look on-chain. $DAI is an example of such stablecoin. It’s trusted by a huge community of crypto investors and developers.

Algorithmic stablecoins

They are typically minted & issued by a DeFi protocol and are commonly under-collateralized (meaning they aren’t backed by an equivalent or excess amount of collateral). Instead, they mostly rely on an algorithm that aims to maintain a stable price by expanding & contracting the stablecoin’s supply.

The intent is to influence interest rates and market behavior, which, in theory, ultimately return the stablecoin to its target price. The key promise is that the algorithm & incentive mechanisms work as promised, & the stablecoin maintains its peg through the issuance & removal of its supply.

The downside: The non-collateralized, algorithmic model keeps failing. Luna UST is one such example.

Historically, the adoption of Fiat-collaraterized stablecoin has dominated this segment, with over 95% of the market share, some economists even call it “Smart Money”.

What does the future hold?

Stablecoins definitely have the potential to play a pivotal role in the global economy and the future of digital finance.

Once we see central banks, regulators and the traditional financial sector starting taking notice which they already have. They could bring a host of benefits into this sector. The pros of stablecoins are obvious: Low-cost, safe, real-time and more intuitive and competitive with what the consumers and businesses need today.

They could rapidly change and make it cheaper for businesses to accept payment, for governments to run cash intensive programs and connecting the unbanked population.

Hello readers! Hope you liked what you read today. Click the like button at the bottom of this page and share insights with your colleagues and friends!

For more such amazing content like and follow Digilah

It is a paradox of our lives that some of the most common of actions underlying a functioning society are left virtually untouched by advancement as civilization marches forth to Metaverses and recyclable rockets. An example is how Education has operated historically – a source of knowledge (teacher/computer) facing a collective of students, dispensing knowledge. The dispenser may vary but the fundamental construct remains unaltered. But the one I want to focus on today is the act of making Payments. Yes, payments…the industry that is supposedly being disrupted with an onslaught of payment tech start-ups touting nosebleed valuations. But if one peels away the slick interface and looks into exactly how the payments course from one end to the other, you will inevitably run into technology which was built when Mash was still on air and “Bloody” a bad word!…

Let’s think of a situation where a corporation say Nike, needs to pay its suppliers in Vietnam called VietShoe. Nike instructs it’s bank to make a payment in VND to its supplier bank account. Nike is shown a FX rate by the trader at Nike’s bank, “Banque de Zapatas”(BDZ)…there follows a little negotiation… then finally the golden word “done” is said/typed. The next stage is for the operations people then deduct the USD100 from Nike’s account in the US and initiate a series of steps whose desired outcome is to get the VND equivalent of USD100 (about 2,250,000 VND at current rates) credited to VietShoe’s account.

FX markets are the largest component of capital markets with a daily trade volume is 6.6 Trillion USD (the equivalent number for equities is 0.5 T and bonds is 4.7T). hence, there are hundreds of thousands of such Nikes making millions of payments to the Vietshoes of the world every day! The scale is mind boggling. The good news is that there is a method to the madness. There is a common platform and a common language which banks can speak to each other. And a central organization creating rules for this superhighway, so these trillions can move around seamlessly. That organization is a member owned cooperative called SWIFT (Society for Worldwide Interbank Financial Telecommunication). This was set in the 70s! And is still the backbone of the vast majority of the 6.6T being transacted every day.

% Turnover

I will give you a brief taste of the gymnastics involved in the example above.

1.Once the rate is agreed with Nike, Bank NY needs to let it’s partner bank in Vietnam called Bank VN (termed “onshore bank” in the Trading Room) two things – One, the identity of the Beneficiary and it’s bank account details and Two, the amount to be transferred. This is done using a MT 103 Swift format file.

2. Once Bank VN receives the request, it will debit the account BDZ maintains with it for 2,250,000 VND and credit the ultimate beneficiaries account.

(I am making a number of simplifying assumptions here like the presence of “nostro” account as well as absence of routing banks. These can be the subject of another future note.)

The route above, is how most fintech apps work today. If evaluated by a tech person, she will be aghast at the usage of flat files, and, in a minority of cases, API calls (which will be the subject of future write ups). Now, take a step back and juxtapose the promise of blockchain technology to this archaic construct… suddenly, The Swift system, if imagined as an entry on a vast netted ledger, across multiple counterparties, begins to resemble a classic blockchain construct. And the realization comes that this is the exact point where the technology should be deployed and has not, for the most part, been deployed. For it remains mired in producing Dogecoin’s and NFTs to make use of those Dogecoins!!